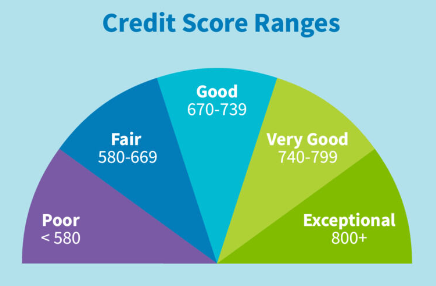

How to build a good credit score?

Building a good credit score requires responsible financial habits. Start by paying your bills on time and in full each month to demonstrate reliability. Keep credit utilization low by using only a portion of your available credit. Maintain a healthy mix of credit accounts, including credit cards, loans, and a mortgage if possible. Avoid opening too many new accounts at once. Regularly monitor your credit report for errors and address them promptly. Patience and consistency in practicing these habits will help you build a solid credit history and improve your credit score over time.

Pay Bills on Time: Timely Payments for a Strong Credit History

Paying bills on time is a crucial factor in building a good credit score. Late or missed payments can have a negative impact on your credit history and lower your score. To establish a strong credit history, make it a priority to pay all your bills, including credit card bills, loan installments, and utility bills, by their due dates. Consider setting up automatic payments or reminders to ensure timely payments. Consistent on-time payments demonstrate your reliability and financial responsibility, which are key factors in maintaining a positive credit history and improving your credit score over time.

Manage Credit Utilization: Keeping Balances Low

Credit utilization refers to the amount of credit you use compared to your total available credit. It is recommended to keep your credit utilization ratio below 30% to maintain a good credit score. To manage credit utilization effectively, aim to keep balances low on your credit cards and revolving credit accounts. Avoid maxing out your credit cards or carrying high balances. Regularly review your credit card statements and make payments to reduce outstanding balances. By managing your credit utilization responsibly, you demonstrate your ability to use credit wisely, which positively influences your credit score.

Maintain a Mix of Credit: Diversifying Your Credit Portfolio

Having a mix of credit accounts can positively impact your credit score. Lenders like to see that you can handle different types of credit responsibly. It’s beneficial to have a combination of credit cards, loans (such as auto loans or personal loans), and a mortgage if applicable. However, it’s important to only take on credit that you can manage responsibly. Having a diverse credit portfolio showcases your ability to handle various credit obligations and can contribute to a higher credit score over time.

Avoid Opening Multiple Accounts: Moderate Approach to New Credit

While having a mix of credit is beneficial, it’s important to avoid opening multiple accounts within a short period. Opening several new accounts can raise concerns for lenders and may negatively impact your credit score. Each time you apply for new credit, it results in a hard inquiry on your credit report, which can temporarily lower your score. Instead, take a moderate approach to new credit, only opening accounts when necessary and when you can manage them responsibly.

Monitor and Correct Errors: Regularly Check and Address Inaccuracies

Regularly monitoring your credit report is essential for maintaining a good credit score. Obtain a copy of your credit report from each of the major credit bureaus (Equifax, Experian, and TransUnion) and review it for any errors or inaccuracies. Incorrect information on your credit report can negatively impact your score. If you find any errors, such as accounts that don’t belong to you or incorrect payment information, dispute them with the credit bureaus to have them corrected. By monitoring your credit report and addressing errors promptly, you can ensure that your credit history is accurately reflected, leading to a stronger credit score.

FinancesGlad is India’s fastest growing online publication Blog for Entrepreneurs, Small business, Bloggers and personal finance experts.